Decoding the ASX Big Names

Australia's largest conglomerate: Opportunities and challenges for Wesfarmers

When it comes to conglomerate names, US investors often think of $Berkshire Hathaway-B (BRK.B.US)$ , led by the renowned billionaire investor, Warren Buffett.

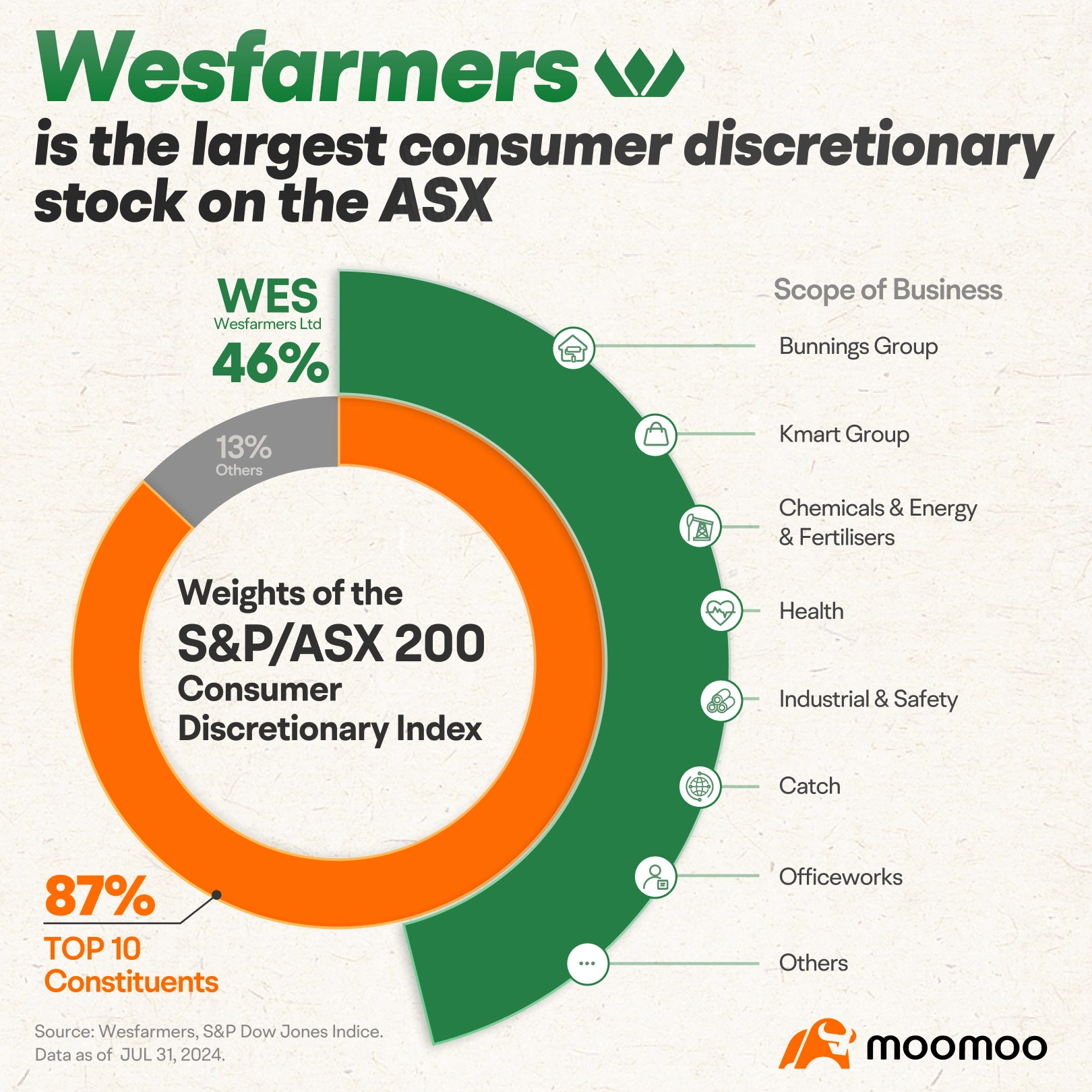

In Australia, the most prominent conglomerate name would be $Wesfarmers Ltd (WES.AU)$ , which has an extensive range of businesses spanning retail, chemicals, energy, fertilisers, health, office, industrial and safety products. Notably, it is the largest consumer discretionary stock on the Australian Securities Exchange (ASX) by market capitalisation, and one of Australia's largest private sector employers.

Although Wesfarmers may not be a widely recognised name across the country, it has an extensive portfolio of underlying businesses that include many well-known brands, such as Bunnings, Kmart, Target and Officeworks.

In this article, we'll take a closer look at the retail conglomerate, whose shares are owned by over 500,000 shareholders.

Business divisions

Established in 1914, Wesfarmers originated as a cooperative aimed at assisting farmers in Western Australia with the cultivation and marketing of their produce.

In 1984, it transitioned into a public company and embarked on a series of strategic acquisitions, expanding its presence in diverse industries. As a result, Wesfarmers has transformed into a holding company and emerged as one of Australia's largest publicly listed companies.

As of the 2023 financial year, Wesfarmers' major business divisions include:

● Bunnings Group is the leading retailer of home improvement and lifestyle products in Australia and New Zealand, and a major supplier to project builders, commercial tradespeople and the housing industry. It is one of Australia's most trusted retail brands, supported by its commitment to lowest prices, widest range and best experience along with a unique capacity to expand its addressable market.

● Kmart Group comprises retail business Kmart and Target, with operations across 449 stores in Australia and New Zealand. Kmart and Target are supported by KAS Group Asia through direct sourcing and global wholesale operations.

● Chemicals, Energy and Fertilisers manages nine businesses in Australia across the chemicals, energy, fertilisers and lithium sectors with a shared services model that supports businesses across the portfolio.

● Officeworks is Australia's leading retailer of stationery, technology, furniture, art supplies, and learning and development resources, with more than 40,000 products available online as well as services like Print and Create, and Geeks2U.

● Industrial and Safety is a leading supplier of industrial safety and workwear products to a wide range of customers, including Australia and New Zealand's largest corporate and government entities. The division operates three main businesses: Blackwoods, Worwear Group and Coregas.

● Health is formed in March 2022, with the acquisition by Wesfarmers of API, a health wellbeing and beauty company that has served Australians for more than 100 years. It operates as a wholesale distributor to over 2,500 pharmacies across Australia and offers additional retail support services through its Priceline Pharmacy and other franchise partners.

Investment highlights

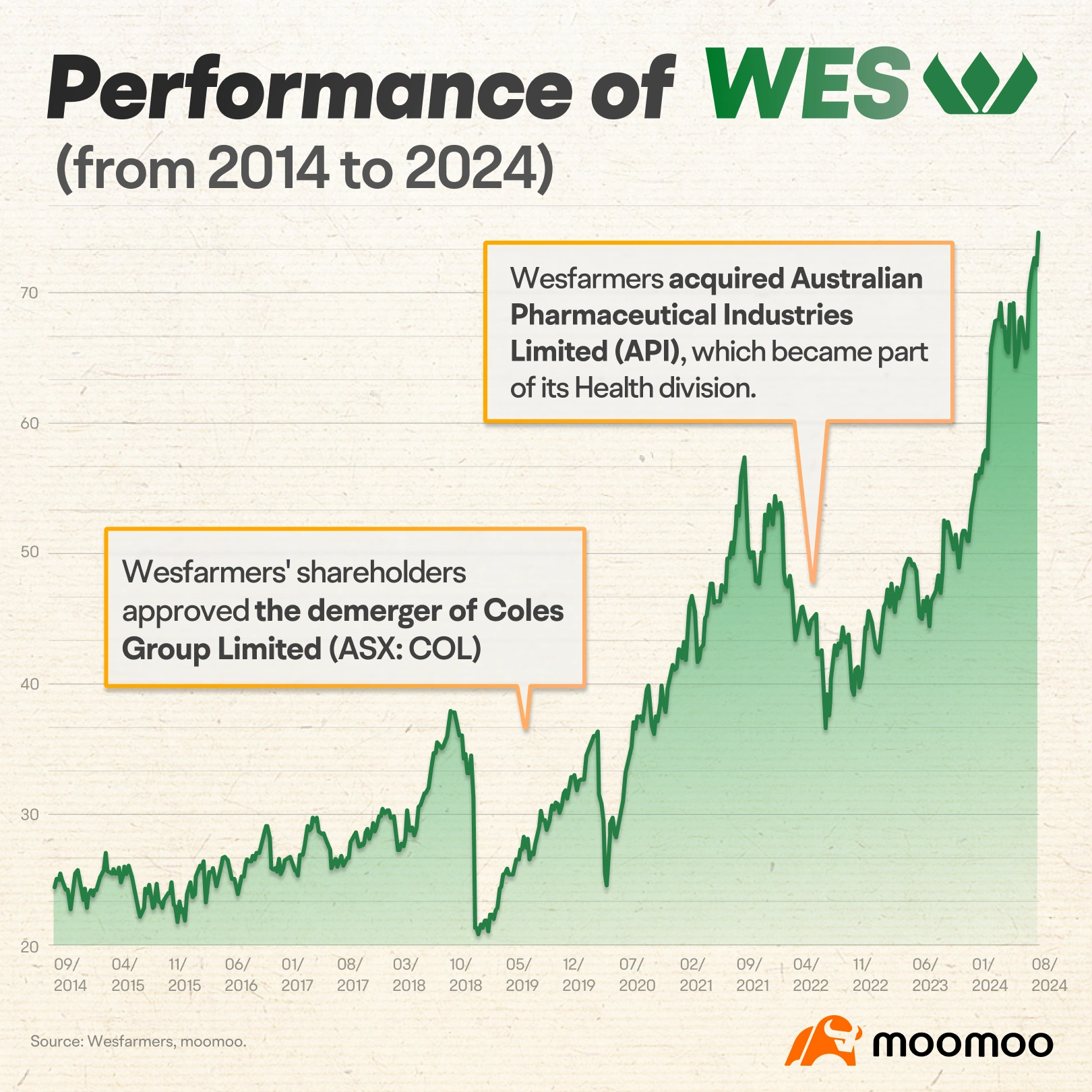

Wesfarmers is committed to achieving a satisfactory return for its shareholders by employing various strategies, including optimising the performance of its businesses and pursuing new avenues of growth. The company has a compelling record of achieving this objective, as evidenced by its share price increasing by approximately 180% over the past decade, not including dividends.

For investors who are studying the retail conglomerate, the following factors may provide valuable insights:

● Diversified operations

Wesfarmers is often regarded by investors as a mini Berkshire Hathaway, owing to its remarkable success. This achievement can be attributed to the company's exceptional diversification across multiple sectors, achieved through an acquisition-driven growth strategy. This approach has allowed Wesfarmers to establish a well-balanced blend of defensive characteristics and growth prospects.

An excellent illustration of Wesfarmers' evolutionary journey is its fertiliser business, which contributed to approximately 60% of its earnings during the company's IPO in 1984. Today, the business accounts for just 1% of Wesfarmers' earnings. Had the company confined itself to a narrow definition of being solely a rural or fertiliser business, it would have missed out on numerous opportunities that have presented themselves over the past few decades.

Wesfarmers' diversified portfolio provides the company with the flexibility to adapt its capital allocation strategy over time. Nevertheless, this diversification can pose challenges for investors seeking to comprehend the various businesses within the company. Consequently, the divisions comprising a conglomerate often experience a reduction in valuation when consolidated.

● Retail dominance

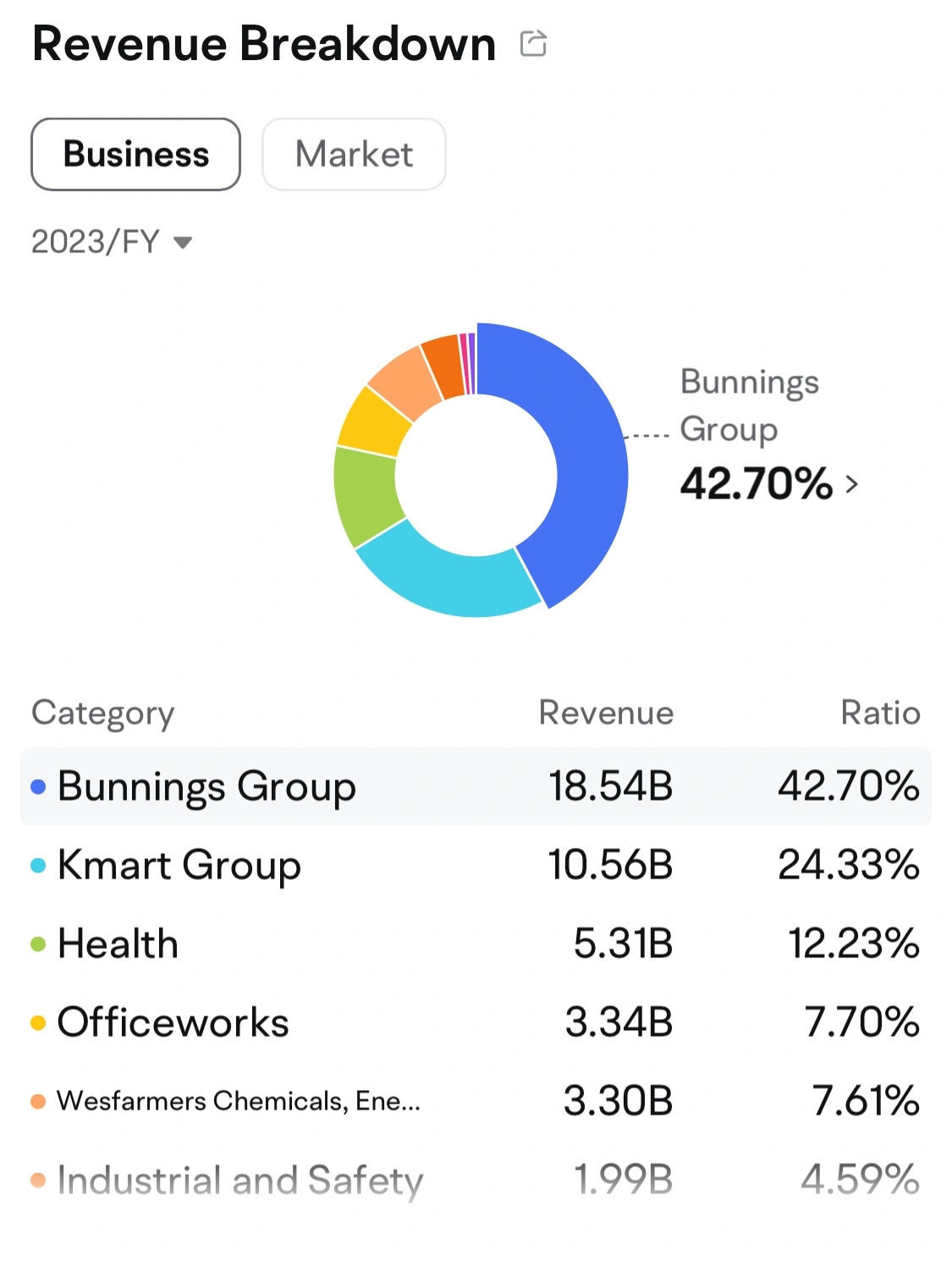

Wesfarmers' portfolio comprises a collection of high-quality businesses, with its biggest and most profitable divisions, Bunnings and Kmart, representing the majority of the company's earnings before tax (EBT).

As per the 2023 financial report, Bunnings accounted for 42.7% of Wesfarmers' total revenue and contributed 57.7% of its EBT. Meanwhile, Kmart generated 24.3% of the company's revenue and 19.9% of its EBT.

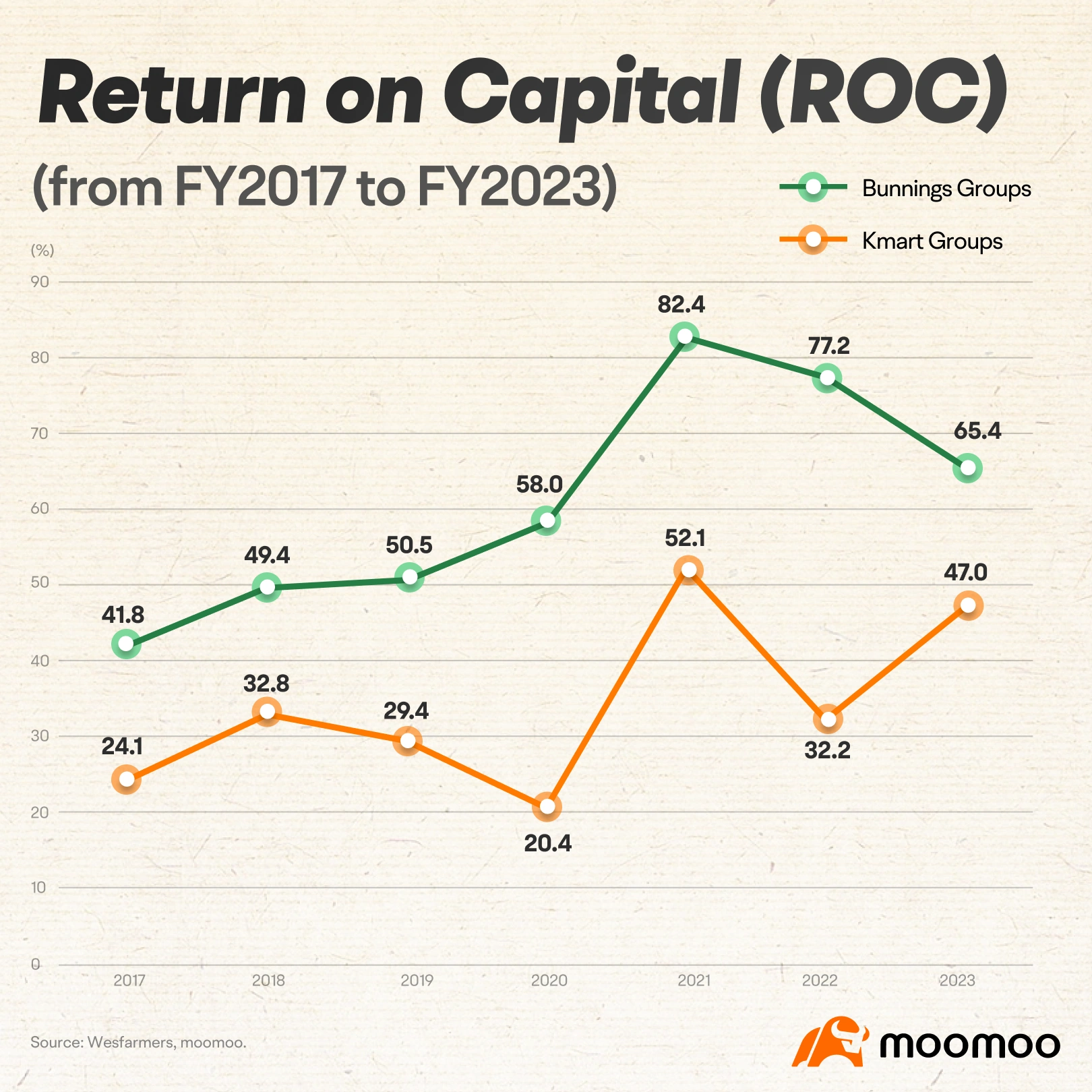

It is worth noting that both Bunnings and Kmart boast impressive returns on capital (ROC), with Bunnings at 65.4% and Kmart at 47.0%, significantly surpassing other divisions. As a result, for every dollar Wesfarmers invests in Bunnings and Kmart, the company generates returns of 65 and 47 cents, respectively, which is a substantial competitive advantage in the retail sector.

In contrast to Kmart, Bunnings represents a more substantial portion of Wesfarmers' portfolio. Nevertheless, Bunnings is susceptible to the cyclical nature of Australian construction activity, with retail sales being highly influenced by the housing market and consumer confidence.

● Future growth avenues

Wesfarmers is actively pursuing new growth areas, such as healthcare and lithium mining, with the potential to create additional revenue streams. This strategic approach could also support the company in sustaining a premium price-earnings (P/E) ratio in the market.

The Health division was formed in March 2022, following the acquisition of API, a leading health and beauty company in Australia. The Health division further expanded its digital and medical aesthetics portfolio in 2023 with the purchases of telehealth provider, InstantScripts, and the SILK Group, a network of approximately 140 wholly-owned, joint venture and franchised clinics.

The 2023 financial year marked the first full year of operation for Wesfarmers' Health division, which delivered improved earnings of $45 million on revenue of $5,312 million.

In addition to the Health division, Wesfarmers has also invested in Covalent Lithium, in which it holds a 50% stake. Wesfarmers has made significant investments in lithium production through the Covalent lithium project, which features a large-scale, long-term, and high-grade lithium hydroxide facility in Western Australia.

The lithium business stands as a pivotal growth platform for Wesfarmers, offering long-term value to shareholders and capitalising on worldwide decarbonisation initiatives. Earnings from the lithium business are expected to commence in the first half of the 2024 financial year from the sale of interim spodumene concentrate.

● Financial performance

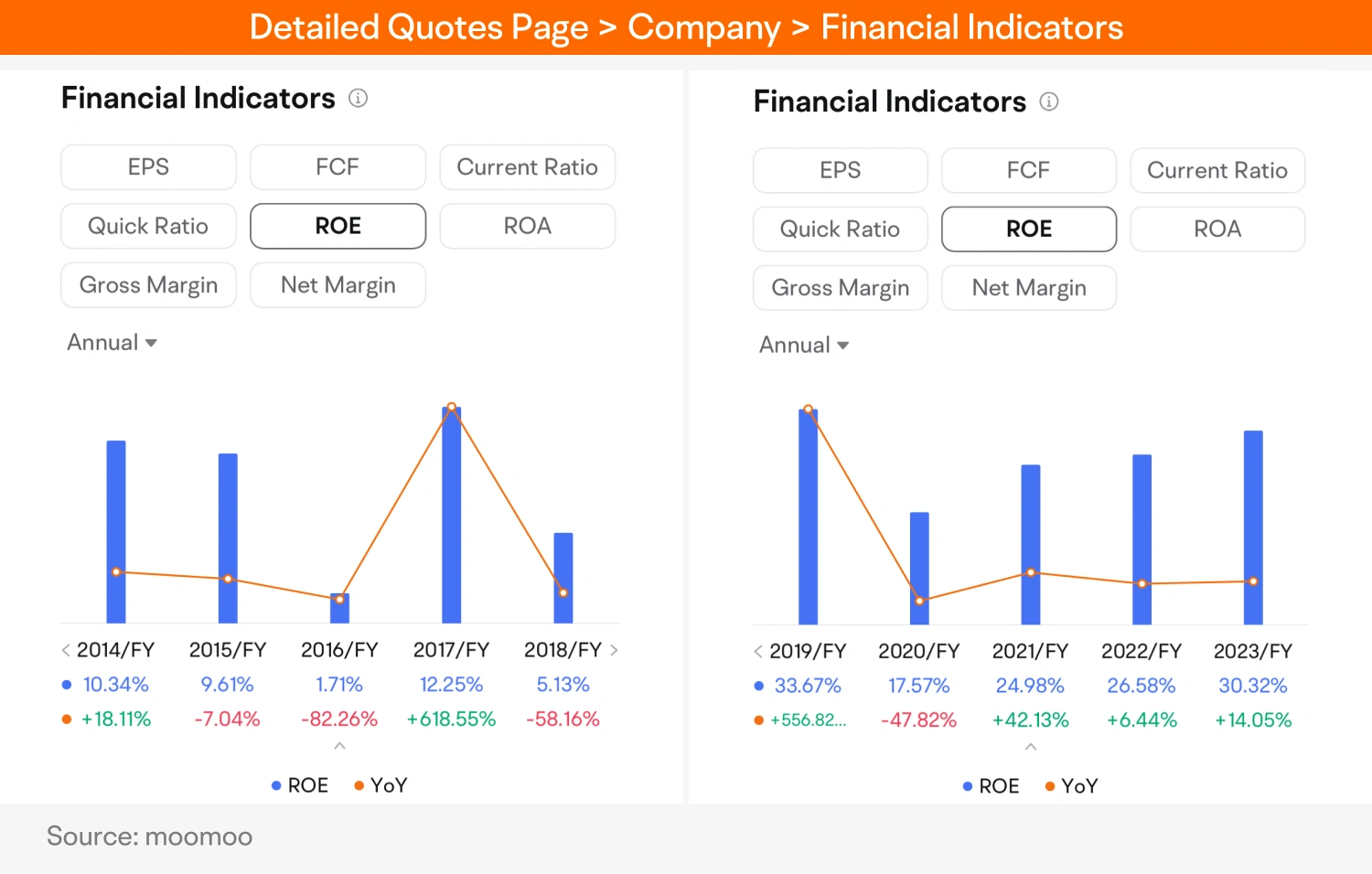

Wesfarmers' primary objective is to deliver satisfactory returns to shareholders over the long term. To assess this goal, the company focuses on return on equity (ROE) as a key internal performance indicator. This metric gauges the company's ability to generate returns on the investment it received from shareholders.

Wesfarmers has achieved impressive ROE in recent years, notably after its demerger of Coles Group Limited (ASX: COL) in the 2019 financial year. This was the largest demerger in Australian corporate history, resulting in significant impacts to Wesfarmers' financial results.

While ROE is recognised as a fundamental measure of financial performance at a Group level, Wesfarmers has adopted return on capital (ROC) as the principal measure of performance for the divisions. ROC provides a comprehensive evaluation of a company's effectiveness in capital allocation. This was exemplified in 2018 when Wesfarmers spun off Coles Group Limited, driven in part by the objective of optimising capital usage in relation to the generated profits.

Wesfarmers' two prominent retail divisions, Bunnings and Kmart, have exhibited exceptional and improving ROC over the past few years.

● Valuation

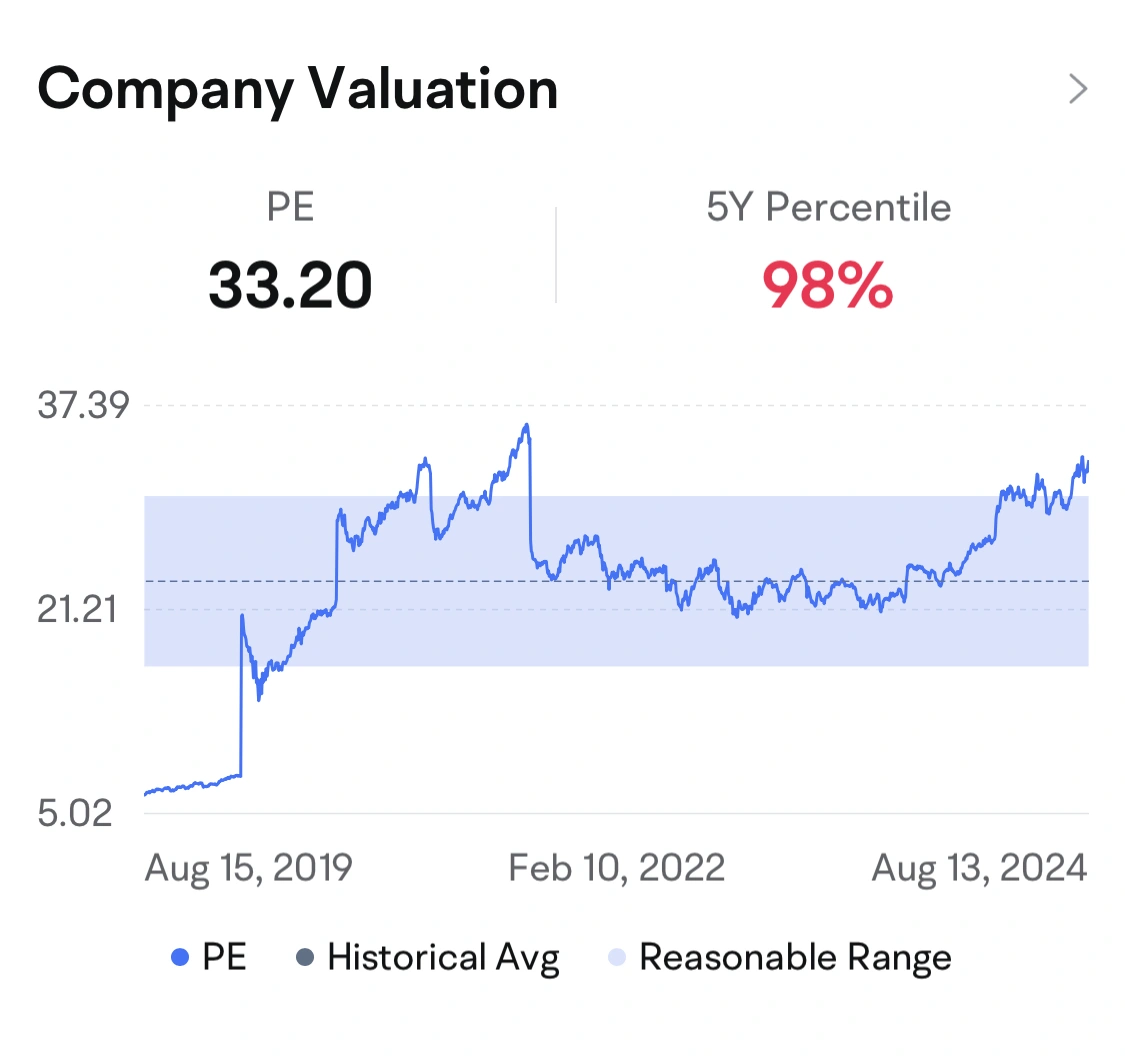

When a company's share price outpaces its profit growth, it leads to an increase in the price/earnings (P/E) ratio. This suggests that the stock is being traded at a higher multiple of its earnings, making it relatively more expensive.

As of 14 August, 2024, Wesfarmers had a P/E ratio of 33.20, surpassing the industry average and significantly exceeding its historical levels. This was primarily driven by the company's surging share price, which rose by 28.9% in 2023 and continued to climb by 30.56% year to date.

Although Wesfarmers' P/E valuation may appear expensive, this can be attributed in part to the high expectations regarding the company's performance and growth potential. Specifically, there is optimism surrounding its future growth avenues, such as healthcare and lithium mining.

The bottom line

The key to Wesfarmers' success lies in its steadfast commitment to delivering satisfactory returns to shareholders over the long term. This objective directs its strategies towards the creation of shareholder wealth, rather than expanding its empire.

To achieve outstanding shareholder returns, Wesfarmers focuses on investing in opportunities with high or improving ROC. Despite facing certain hurdles in its business development history, the company's impressive track record of delivering shareholder returns speaks for itself.

Some investors view Wesfarmers as a miniature version of Berkshire Hathaway, given its status as a diversified conglomerate. However, the difference lies in the fact that most of Wesfarmers' businesses are wholly-owned, whereas Berkshire is increasingly taking portfolio stakes in its investments.